How Much Salary Should I Save?

“How much salary should I save?” Do I need to save from my already overstretched salary and overwhelming budget? Saving money is one of the most important financial habits you can develop.

But how much of your salary should you save each month? This question does not have a one-size-fits-all answer, as it depends on various factors such as income level, expenses, financial goals, and lifestyle choices.

Here’s the deal:

Many financial experts recommend saving at least 20% of your monthly income, but your actual savings rate should be tailored to your unique situation.

Whether you are saving for an emergency fund, a significant purchase, or long-term financial security, understanding how much to set aside can make a substantial difference in your financial future.

Now, you may be wondering:

- What’s the ideal salary savings percentage?

- How much should I save each month?

- What strategies can help me save more effectively?

The bottom line?

Your savings plan should align with your income, expenses, and long-term financial objectives.

In this guide, we’ll break down recommended savings guidelines, clever budgeting techniques, and factors that affect how much you can realistically save—so you can make the most of your hard-earned money.

Understanding Savings Goals

Before deciding how much your salary to save, you must understand your financial goals.

Saving money isn’t just about setting aside a percentage of your income—it’s about planning for both short-term needs and long-term security.

But why do savings goals matter?

Because they give you a clear purpose and direction, saving money can feel overwhelming without defined goals, and you may struggle to stay consistent.

Also Read:

Why Saving a Portion of Your Salary Is Important

You may be wondering:

Why should I prioritise saving money when I have so many expenses?

Here’s the deal:

Savings act as a financial safety net. Whether it’s an emergency fund, retirement planning, or a major purchase, having money set aside ensures you’re prepared for life’s unexpected events.

For example, research by The Money Charity UK found that 9.3 million people in the UK have no savings, leaving them financially vulnerable in an emergency.

Now, let’s break down the key reasons why saving is essential:

- Financial security—A well-funded emergency savings account can help cover unexpected expenses, such as medical bills or car repairs.

- Debt prevention – Having savings prevents reliance on credit cards and loans, reducing financial stress.

- Retirement planning – The earlier you start saving, the more you can benefit from compound interest.

- Future investments—Savings give you more financial flexibility, whether buying a home, starting a business, or pursuing further education.

What Percentage of Your Salary Should You Save?

Now, let’s get to the big question: how much salary should I save?

A general rule of thumb is to aim for at least 20% of your income, based on the 50/30/20 rule in the UK. But here’s the kicker—your savings rate should be flexible, depending on your financial situation.

Here’s a simple breakdown:

- If you’re starting, saving 10-15% of your salary is a good goal.

- With a stable income, aim for the recommended 20% or more.

- Focused on early retirement? Saving 30-50% of your income can accelerate financial freedom.

But what if you can’t afford to save 20% right now?

That’s okay! The key is to start small and increase your savings over time. Even saving 5% of your salary is better than nothing.

Let’s explore how to structure your savings to meet different financial goals.

See Also:

Short-Term vs. Long-Term Savings Strategies

Not all savings should be treated the same. How you save depends on your goals and how soon you’ll need the money.

Here’s how you can do the same thing:

- Short-term savings (0-5 years): Ideal for an emergency fund, travel, or major purchases like a car.

A high-interest savings account in the UK can help grow your money while keeping it accessible.

- Long-term savings (5+ years): Best for retirement savings in the UK, home buying, or future investments.

Investing in pensions or ISAs can offer better returns than a traditional savings account.

The bottom line?

Understanding your salary savings percentage for each goal ensures your money is working for you efficiently.

Recommended Savings Guidelines

There is no one-size-fits-all approach to savings. However, financial experts suggest specific guidelines to help structure your savings efficiently.

Let’s explore some of the most widely recommended savings methods.

The 50/30/20 Budget Rule Explained.

One of the most popular budgeting frameworks in the UK is the 50/30/20 rule. But what is it, exactly?

Here’s how it works:

- 50% of your income goes to necessities (rent, utilities, groceries, transportation).

- 30% is allocated to wants (entertainment, dining out, subscriptions).

- 20% is reserved for savings and debt repayment.

But why is this rule so effective?

Because it ensures a balanced approach to money management, you create a financial cushion by consistently saving 20% of your salary while still enjoying life.

For example, if you earn £2,500 per month, using the 50/30/20 rule UK would mean:

- £1,250 for essentials

- £750 for discretionary spending

- £500 for savings and debt payments

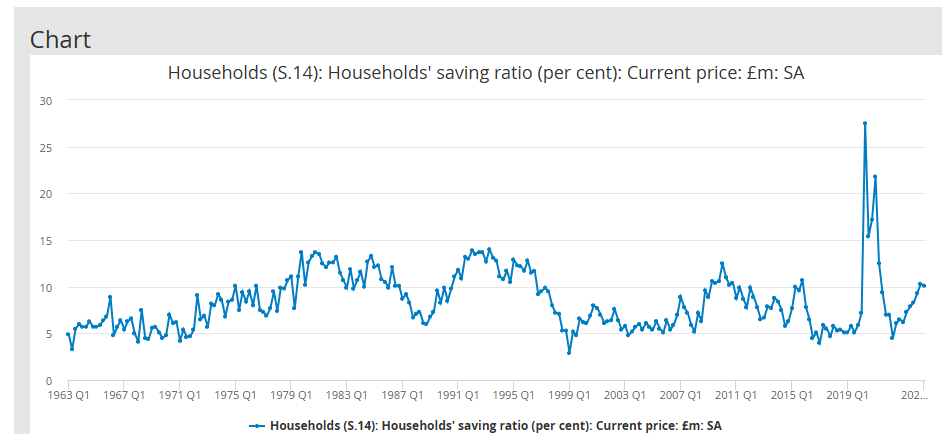

According to the Office for National Statistics (ONS), the average UK savings rate was 8.7% in 2023. While this is below the 20% recommendation, it’s a good starting point for those struggling to save.

Read Also:

How Much to Save for Emergencies

Now, let’s discuss your financial safety net—your emergency fund.

Experts recommend having at least three to six months’ worth of living expenses saved in case of unexpected situations like job loss or medical emergencies.

But what does that look like in real numbers?

- If your monthly expenses are £2,000, aim for an emergency fund UK target of £6,000 to £12,000.

- If you’re self-employed or have an irregular income, saving nine to twelve months’ worth may be safer.

But what if you’re starting from zero?

Begin with a small goal, like saving one month’s expenses, and gradually build from there.

A study by The Money and Pensions Service found that 22% of UK adults have less than £100 in savings. This shows how crucial it is to start an emergency fund immediately.

Retirement Savings: How Much Is Enough?

You may be wondering:

How much should I save for retirement in my 30s?

Here’s the deal:

The sooner you start, the better. Thanks to compound interest, even small contributions can grow significantly over time.

The general guideline for retirement savings in the UK is:

- By age 30: Have at least one year’s salary saved.

- By age 40: Aim for three times your annual salary.

- By age 50: Target six times your salary.

For example, if you earn £35,000 per year, your retirement fund goal by age 40 should be around £105,000.

But what if you’re behind on savings?

It’s never too late to start. Increasing contributions to your pension or opening a high-interest savings account in the UK can help you catch up.

Read Also:

Factors That Affect Your Savings Rate

While general guidelines provide a good starting point, your circumstances greatly determine how much of your salary to save.

Income Level and Cost of Living Considerations

Your ability to save is directly tied to your income and living expenses. Someone earning £60,000 in London will have different savings potential than someone earning £25,000 in Manchester.

Here’s an example:

- You can allocate more to savings and investments if your salary is high.

- If you’re in a high-cost area, you might need to adjust your savings goals based on rent and daily expenses.

A recent study by the Resolution Foundation found that the UK’s cost-of-living crisis has impacted savings habits, with many struggling to set aside even 5% of their income.

Debt Repayment vs. Savings – Striking the Right Balance

But what if you have debts? Should you save or pay off debt first?

The answer depends on your financial situation. A balanced approach is often the best strategy:

- High-interest debt (credit cards, payday loans) – Prioritise repayment first before aggressive saving.

- Low-interest debt (student loans, mortgages) – Continue saving while making regular debt payments.

For example, if you have a credit card balance with a 20% interest rate, paying it off should take priority over saving.

How Lifestyle Choices Impact Your Savings Potential

Your lifestyle and spending habits can either support or hinder your savings goals.

Consider these questions:

- Do you eat out frequently or cook at home?

- Do you prioritise luxury purchases over financial security?

- Are you living within your means?

Making minor adjustments—like reducing impulse purchases or switching to a more affordable phone plan—can free up extra money for savings.

The bottom line?

Your savings potential isn’t just about income; it’s also about how you manage your expenses.

Practical Tips to Boost Your Savings

Saving money can feel overwhelming, especially with daily expenses and unexpected costs. But the good news is that small changes can make a big difference.

Here’s how to increase your savings without drastically changing your lifestyle.

See Also:

How to Automate Savings for Consistency

One of the easiest ways to build savings is to automate the process. When you set up automatic transfers, you don’t have to rely on willpower—it happens without you thinking about it.

Here’s how you can do the same thing:

- Set a standing order from your main account to a dedicated savings account.

- Use banking apps that round up your spending and save the difference.

- Adjust the transfer amount as your salary increases.

For example, if you transfer £100 automatically each month into a high-interest savings account, you could save £1,200 in a year—without even noticing.

Best High-Interest Savings Accounts in the UK

Choosing the correct savings account can help your money grow faster. High-interest savings accounts in the UK offer competitive rates, allowing you to earn more without extra effort.

Some of the best options currently available include:

- Easy-access savings accounts allow withdrawals anytime but may have lower interest rates.

- Fixed-term savings accounts offer higher interest but lock your money in for a set period.

- Cash ISAs – These are Tax-free savings accounts that can boost your returns.

Before opening an account, compare interest rates, withdrawal limits, and fees. Websites like MoneySavingExpert regularly update the best high-interest savings accounts in the UK.

Investing vs. Saving: Where Should Your Money Go?

This is where many people get stuck—should you save or invest?

Here’s the deal:

- Saving is ideal for short-term goals, emergencies, and guaranteed returns.

- Investing is better for long-term growth but carries some risk.

For example, a high-interest savings account is the safest option if you need money for a house deposit in two years. But if you’re planning for retirement in 20 years, investing in stocks or a pension fund may provide higher returns.

The bottom line?

A balanced approach—saving for security and investing for growth—is the best strategy for financial success.

Conclusion

Saving a portion of your salary is one of the most intelligent financial decisions you can make. Whether you follow the 50/30/20 rule, build an emergency fund, or plan for retirement, having a clear savings strategy can set you up for long-term stability.

You can maximise your financial potential by automating your savings, choosing high-interest accounts, and balancing saving with investing.

But what if you’re looking for more than just financial security? What if you’re preparing for your next big career move?

That’s where RKY Careers comes in.

At RKY Careers, we provide expert interview preparation services to help you land your dream job.

From crafting compelling answers to handling tricky interview questions, we ensure you’re fully equipped to impress recruiters and hiring managers.

Want to boost your career prospects? Contact RKY Careers today and take the next step toward professional success!

FAQs

What is a good percentage of salary to save each month?

A common rule of thumb is to save at least 20% of your monthly salary, following the 50/30/20 rule. However, this percentage can vary based on income, expenses, and financial goals. If 20% isn’t feasible, start with a smaller percentage and gradually increase it over time.

How much should I save for retirement in my 30s?

Experts recommend saving at least one to two times your annual salary for retirement by your mid-30s. According to a report, a moderate pension in the UK requires around £23,300 per year, meaning consistent contributions to a retirement or investment fund are crucial.

Is it better to save or invest my salary?

It depends on your financial goals. Saving is best for short-term needs, emergency funds, and guaranteed returns, while investing is ideal for long-term wealth growth. Investing in pensions, stocks, or ISAs can help your money grow faster if you have a stable emergency fund.

How can I save money on a low salary?

Even with a low salary, small savings add up over time. Start by:

- Cut unnecessary expenses like subscriptions you don’t use.

- Using budgeting apps to track spending.

- Automating small savings amounts.

- Find a high-interest savings account to maximise returns.

Even saving £10-£20 per week can grow into a significant fund over time.